GREENSBORO, N.C. — Having an emergency fund can help smooth out life’s financial hits, whether they’re caused by inflation, unemployment, or being laid up by illness. And as Consumer Reports explains, starting one might not be as tough as it seems.

If you’re lucky, things are going well right now. You have a steady paycheck, you pay your bills on time, and you may even have a little extra money left over.

But what if something unexpected happens? We’ve all experienced financial emergencies, like major home repairs, medical bills, or even the loss of income.

"Having a rainy day fund to cover these types of unplanned expenses can protect you from major debt, which can easily turn into a financial crisis," said Lisa Gill of Consumer Reports

Many financial planners say that putting aside enough to cover three to six months of essential expenses is a good rule.

"That’s for housing, food, transportation, and debt repayment. So figure out how much that is on a monthly basis, then multiply it by up to six to come up with the amount you should save for your emergency fund," said Nestor Vargas, Certified Financial Planner.

HOW MUCH MONEY SHOULD I PUT IN EACH MONTH?

Once you determine your savings target, don’t let that number daunt you. It’s definitely important to start saving as much as you can. Even if it’s $5 or $10 a month, you’ll be surprised by how quickly that adds up.

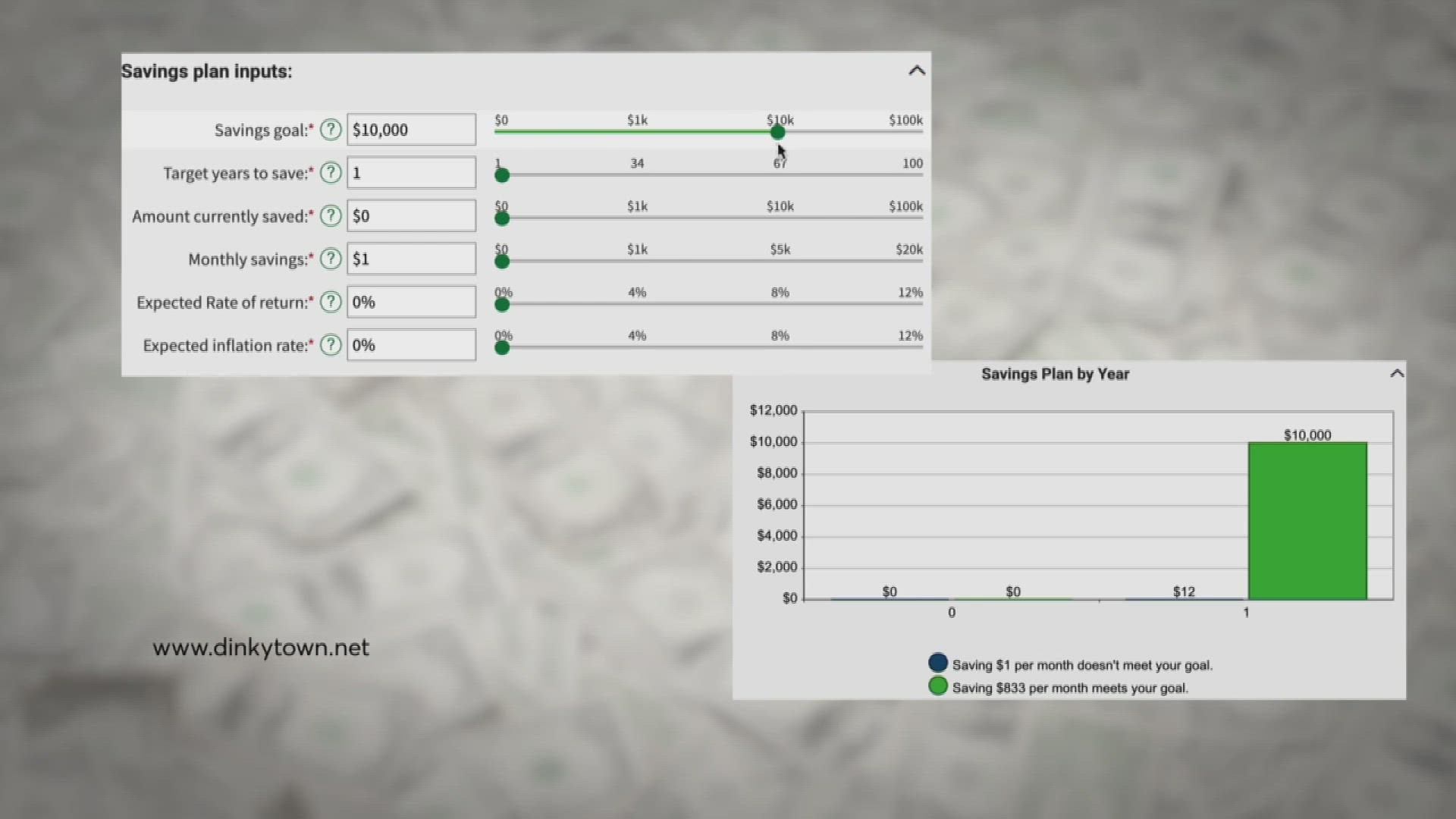

An online savings calculator can show how much you’ll need to set aside each month to reach your goal, and how quickly that money will grow.

Consumer Reports suggests putting the money into a high-yield savings bank or no-penalty certificate of deposit. Many of those accounts now have interest rates of over 4 percent.

THE TRICK TO MAKING SURE THE MONEY GETS INTO SAVINGS

Make saving even easier by setting automatic deposits or transfers from your checking account to your emergency fund. It will keep your contributions on track and secure until you need them.

While building emergency savings should be at the top of your list, you may have other urgent financial obligations, such as high-interest credit card debt. If that’s the case, paying down that debt should become the priority. If you have low-interest debt, you could strike a balance, funneling some of your savings toward paying it, with the rest going toward your emergency fund. For more on paying off credit card debt, go to CR.org.